(Bloomberg) -- China has surged ahead of the US for corporate bond deals in its yuan credit market in recent months, a rare shift that highlights the deepening impact of the two countries’ diverging monetary policies.

Yuan-denominated bond issuance by non-financial firms exceeded that in the greenback in both July and August, a first for two consecutive months, according to Bloomberg-compiled data. The momentum has started building since the Federal Reserve kicked off its tightening cycle in March: Sales of yuan notes, almost entirely by Chinese firms, totaled 2.04 trillion yuan ($306 billion based on exchange rates at the time of deals) between April and August, versus $283 billion of dollar debt worldwide.

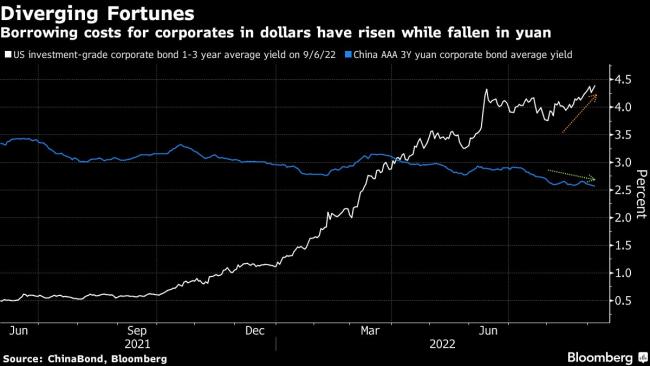

The changing credit market landscape is mostly the result of a plunge in dollar debt sales after the US central bank embarked on a relentless campaign to combat inflation, while Beijing has been doing the opposite to keep funding costs low for an ailing economy. A weakening yuan also bodes well for the trend, even as it dilutes the dollar value of local bonds.

But given the still-minimal foreign exposure to yuan corporate notes, the latest development remains a reminder of the sheer size and weight of China’s economy, rather than the international popularity of its currency, at least for now.

“The rise of yuan corporate debt reflects the divergence of monetary policy between the US and China, and more importantly, liquidity is king,” said Gary Ng, a senior economist at Natixis SA. “But the yuan is still far from challenging the dollar supremacy as most of the yuan bonds are still issued by Chinese firms.”

As the Fed kept on raising interest rates, dollar corporate bond sales have plummeted about 40% to an 11-year low of $592 billion this year as of Sept. 6, with US firms accounting for 76% of them. In contrast, issuance of yuan notes has shed about 6%.

Until this year, it had been rare for yuan corporate bond issuance to outpace that in the dollar for a full month, and the few cases where it did mostly occurred in December due to the Christmas-induced lull.

Cushioning China’s local credit market has been Beijing’s efforts to salvage an economy hurt by a strict Covid Zero policy and an unprecedented property crisis. Authorities have slashed key interest rates and kept the financial system awash with cash, enabling many firms to sell bonds at the cheapest cost in more than a decade.

Meantime, a record wave of defaults by developers and a weakening yuan have made the dollar debt market less accessible or appealing, even for some of China’s stronger firms, giving them added incentives to return home for funding.

However, total dollar debt issuance is still higher than its yuan counterpart for the year and it remains to be seen if Chinese sales can keep up the pace in the coming months. Signs have also started emerging that increased clarity of the Fed’s policy trajectory has persuaded more borrowers to accept the new reality of higher dollar interest rates.

The opening up of its massive domestic bond market has been one of the most tangible and successful liberalization efforts by Beijing in recent years, with the inclusion of Chinese debt into major world indexes bringing in hundreds of billions of dollars from foreign central banks to university endowment funds.

That said, global investors have mostly parked their cash in Chinese sovereign or policy bank bonds, showing continued reluctance to hold local corporate debt amid concerns about an opaque legal system and less reliable onshore credit ratings.

And despite government efforts to promote the yuan-denominated panda bond market, it remains dominated by offshore entities of Chinese firms, with genuine foreign issuers such as the Asian Development Bank and the Polish government being the small minority.

“Credit investors are not afraid of default,” said Jenny Zeng, co-head for Asia Pacific fixed income at AllianceBernstein. “But the challenge in China is that the debt restructuring process after default is not transparent enough.”

©2022 Bloomberg L.P.