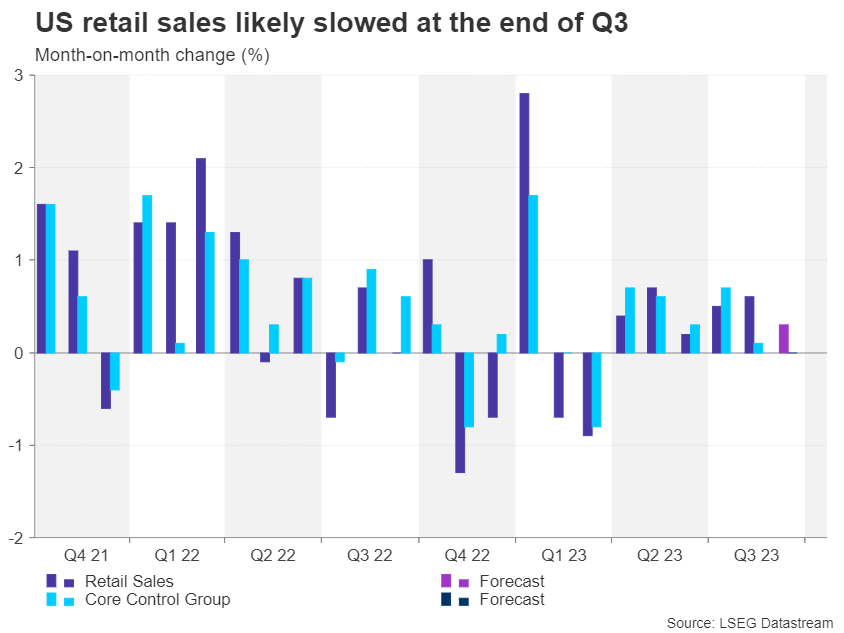

- Retail sales in America likely grew at a more moderate pace in September

- Will the data support a Fed pause in November?

- Or will it fuel the rally in yields and the dollar when it’s out on Tuesday (12:30 GMT)

The US economy has been chugging along quite nicely in 2023 despite hitting several bumps on the road and Fed policy becoming more restrictive than what many investors had anticipated at the start of the year. The Atlanta Fed’s GDPNow forecast model is estimating third quarter growth of 5.1% - that’s well above the recent average of just above 2.0%.

Consumption has been the main driver of this exceptionally strong growth, which is unusual at this late stage of the tightening cycle. This week’s retail sales data will be key in gauging whether consumer spending kept up pace towards the end of the quarter.

After rising by 0.6% month-on-month in August, retail sales are forecast to have grown by a much more moderate pace of 0.3% in September. Excluding automobile sales, retail sales are expected to have edged up 0.2% m/m, while the core figure that strips out gasoline, building materials and food services in addition to autos is projected to have been flat in September, which would suggest households have started to tighten their belts.

Powell may have final say before Fed blackout

Slowing consumer spending isn’t the only risk to growth beyond the third quarter. The possibility of a government shutdown, ongoing strike action and tightening financial conditions could all weigh on growth in the final three months of the year.

The latest round of selloff in US Treasuries and other government bonds has led to a significant tightening in financial conditions, as long-term Treasury yields have surged to pre-financial crisis era levels. More importantly, this hasn’t gone unnoticed at the Fed and officials appear to all be in agreement with one another that the jump in long-term borrowing costs since the last FOMC meeting in September broadly amounts to an equivalent 25-basis-point rate hike.

However, investors have yet to hear from the Fed chief himself, so Jay Powell’s address on Thursday before the Economic Club of New York could be crucial. Powell may well use his speech to guide market expectations before the blackout period for the October 31-November 1 meeting begins at the weekend.

Dollar might shrug off retail sales data

For the markets, the retail sales numbers are not expected to be a game changer as the odds of a November rate hike are virtually zero. However, a stronger-than-expected report on the back of the solid payrolls and CPI readings could nevertheless bolster the case for a December move, or at the very least, lead investors to scale back some of their aggressive bets for rate cuts in 2024.

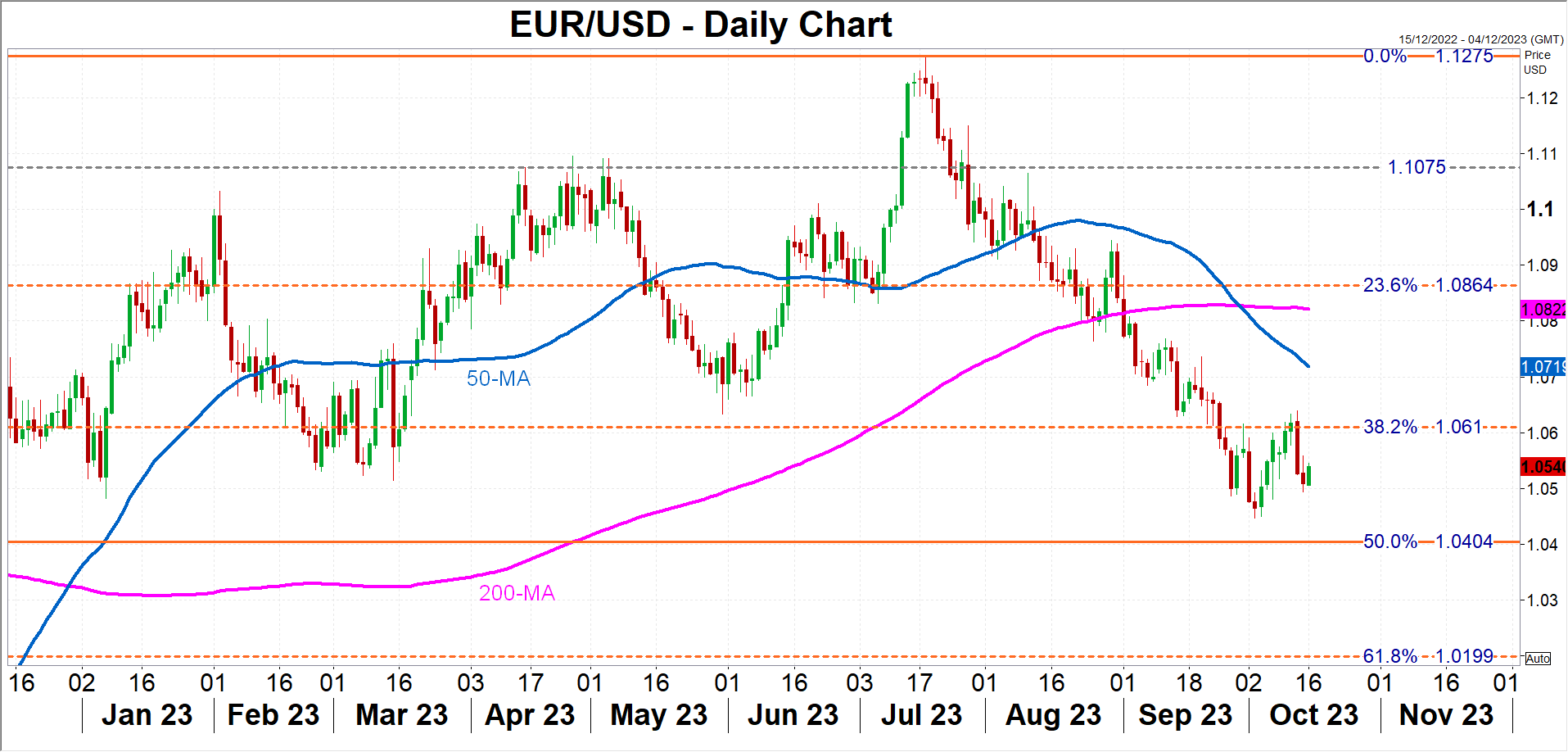

Any fresh boost for the US dollar could push the euro towards the $1.04 level, which marks the 50% Fibonacci retracement of the September 2022-July 2023 uptrend.

But if retail sales disappoint or Powell endorses his colleagues’ views and signals that interest rates have likely peaked, the euro could easily rebound towards its 50-day moving average just above the $1.07 handle.

Safe-haven support for the greenback

Investors should be wary, though, not to completely rule out the chance of another rate hike as a Fed pause is conditional on the 10-year yield remaining elevated near 5.0%, while the Israel-Gaza war is seen as maintaining upside risks to inflation, with oil prices already lifted by the conflict.

The latter even has a two-sided effect on the greenback as it’s generating demand for safe havens. Any pullback in yields might therefore not spark a proportionately sized selloff in the dollar as long as geopolitical tensions are brewing.