- US performs better than other major economies

- After higher Fed rate projections, focus turns to US jobs data

- A still-tight labor market could further lift the dollar

- The data is coming out on Friday, at 12:30 GMT

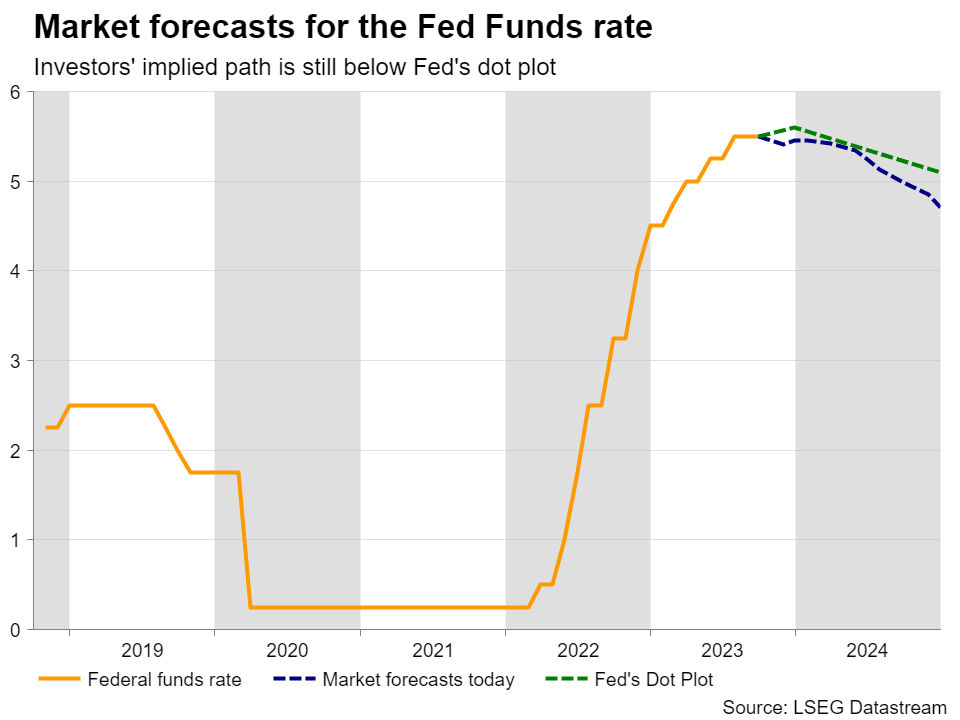

With the US economy proving more resilient than other major ones and inflation rebounding on the back of rallying oil prices, the Fed raised its rate-path projections at its latest gathering, although it did not press the hike button. Specifically, policymakers forecasted one more quarter-point increase before the end of this year, while they saw interest rates ending 2024 at 5.1%, up from June’s projection of 4.6%.

This allowed Treasury yields to climb higher and added more fuel to the dollar’s engines. Although the greenback pulled back at the end of last week, it staged a remarkable comeback on Monday following the better-than-expected ISM manufacturing PMI, suggesting that last week’s retreat was probably due to investors rebalancing their portfolios and hedge funds closing their books for the end of Q3, instead of changing fundamentals.

Will job numbers allow trend continuation?

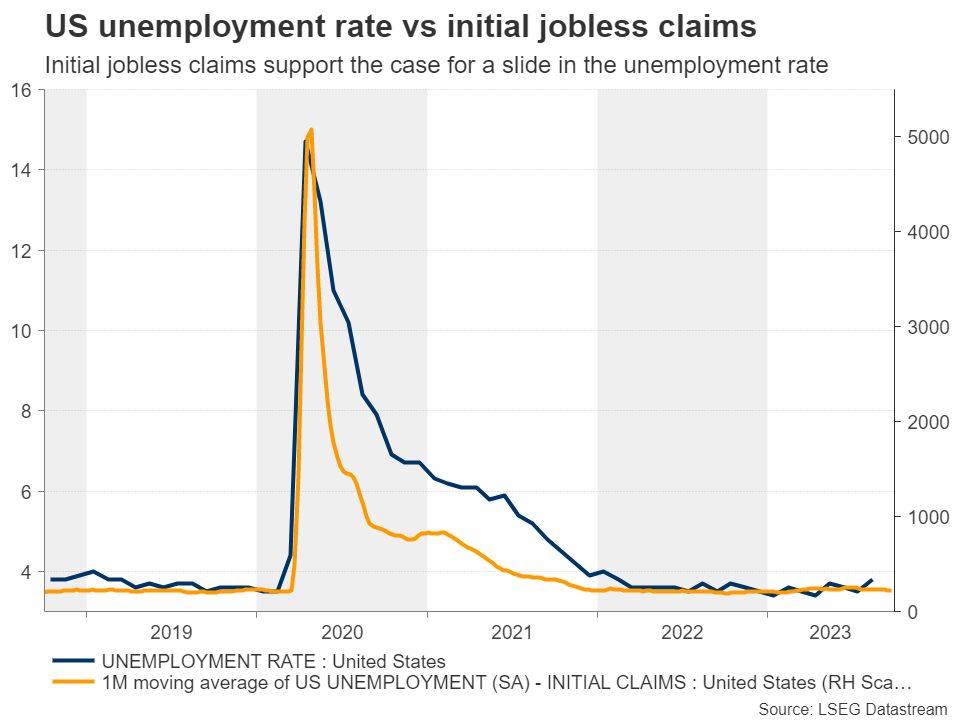

Moving forward, whether this impulsive wave in the greenback’s uptrend will continue may depend on Friday’s employment report. Nonfarm payrolls are expected to have slowed to 163k from 187k, but the unemployment rate is forecast to have ticked back down to 3.7% from 3.8%, which is supported by the modest decline in the 4-week moving average of initial jobless claims.

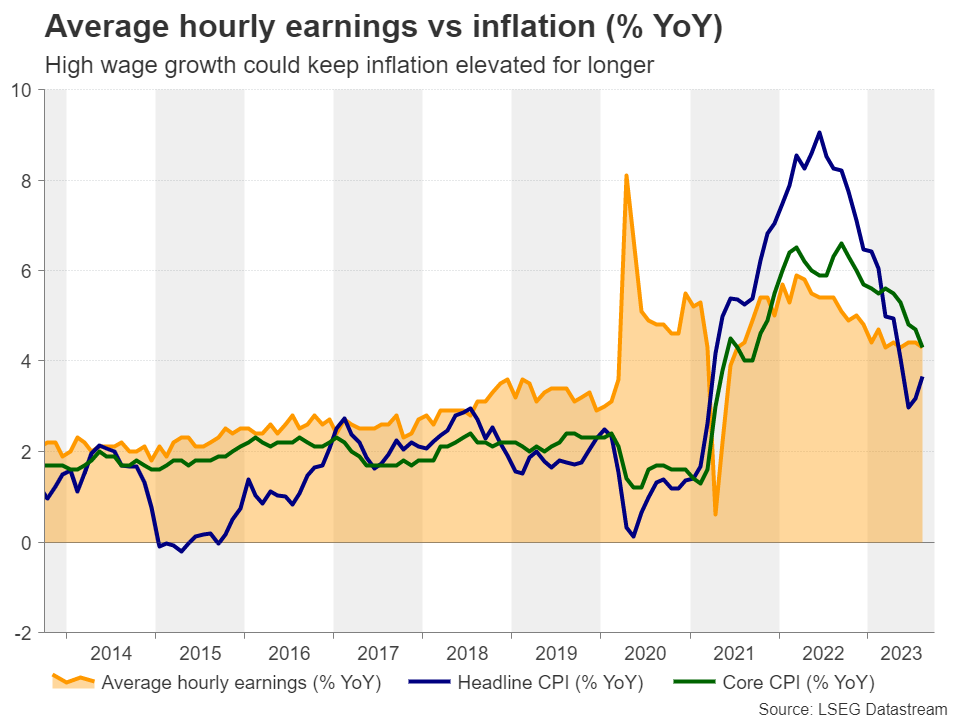

That said, although the initial reaction in the dollar may come from any surprise in the NFPs or the unemployment rate, whether it will be a lasting one could depend on wage growth, which may provide a glimpse of where inflation may be headed in the months to come. Average hourly earnings are expected to have slightly accelerated in monthly terms, keeping the yoy rate steady at 4.3%.

Combined with the uptrend in oil prices, as well as the rebound in headline inflation and projections that the US economy likely performed much better in Q3 than in Q2, elevated wage growth may add to the risk of underlying price pressures intensifying in the months to come.

With investors still projecting a lower rate path than the Fed, assigning only around a 50% probability for another hike and expecting rates to fall to 4.7% by the end of next year, it seems that there is ample room for upside adjustment should Friday’s jobs data come in strong, which could push yields higher and thereby encourage traders to buy more dollars.

At the same time, equities are likely to resume their slide as expectations of ‘higher for longer’ interest rates could exert downside pressure on valuations. Yes, upbeat economic data usually have a positive impact on a nation’s stock market, but the financial community is still in an environment where good news is bad news as it increases the need for additional rate hikes.

Fed not the sole driver

What’s more, expectations about the Fed’s future course of action are not the sole driver of the US dollar and Wall Street. There is also a strong note of uncertainty due to the economic challenges facing China, Eurozone and the UK. And with no other alternative, the only place to seek safety seems to be the US dollar. The yen has long lost its safe-haven status due to the BoJ maintaining a lid on Japanese government bond yields at a time when US rates are keep rising, while gold has fallen victim to both surging yields and a strong dollar, which has lost nearly 6% since September 25.

Euro/dollar keeps printing lower highs and lower lows

Euro/dollar was among the pairs that rebounded decently at the end of last week due to the dollar’s pullback. The rebound happened after the price hit support at 1.0485. However, the pair surrendered those gains on Monday, staying below the downtrend line drawn from the high of July 18 and thereby confirming that the short-term outlook remains negative. The bears managed to push the action slightly below 1.0485 today, and if they are willing to stay in the driver’s seat, a dive towards the low of November 30 at 1.0290 could be possible.

For traders to allow a bigger dollar correction, Friday’s data may need to disappoint. However, even if euro/dollar climbs above 1.0665, the outlook will not turn positive, rather just neutral as the price would be back within the sideways range that contained most of the price action between January 9 and September 22.