· Fed expected to pause again in September

· But will it signal that it is done with rate hikes?

· Risks for the dollar are symmetrical heading into the meeting

· Decision is expected at 18:00 GMT on Wednesday

A pause with strings attached?

The Federal Reserve is widely anticipated to keep interest rates unchanged at its September meeting but what investors are more anxious to find out is whether policymakers will keep the door open to further hikes. The other big discussion point is about the rate path in 2024, specifically, if the median dot plot will be revised higher.

The US economy continues to perform well by most measures even if there are signs of some cooling off, particularly in the tight labour market. With recession odds being slashed and a soft landing looking more attainable, inflation is once again the primary concern for investors and policymakers as how quickly it falls from hereon will determine how soon the Fed can begin cutting rates.

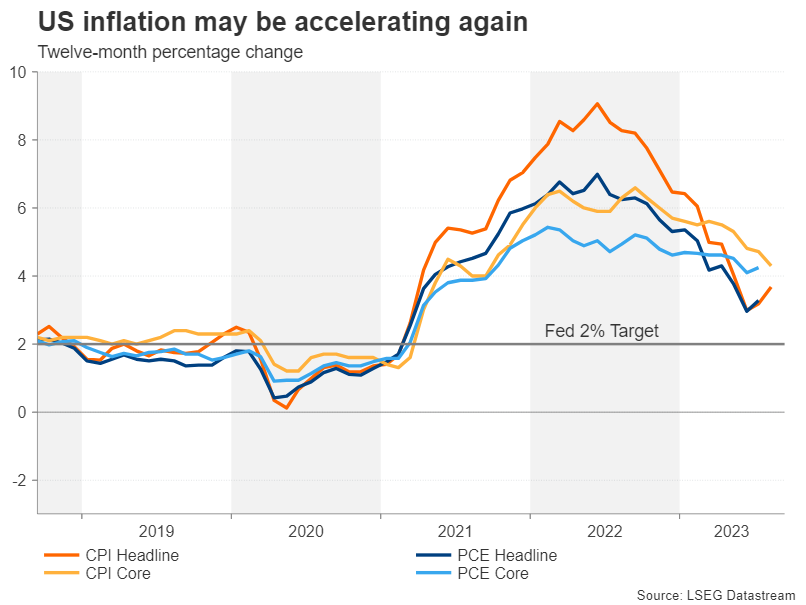

Inflation is creeping up again

Looking at the latest CPI numbers, it’s fair to say that there’s been a bit of a setback in the progress lately. The annual rate of CPI has quickened from 3.0% to 3.7% over the past two months. That trend could continue if oil prices maintain their ascent. However, most investors are looking through this latest increase, hoping that it will be temporary, and focusing on the decline in core CPI for clues as to what the Fed will do next.

Another striking datapoint that markets are not overreacting to is the big jump in consumption over the summer, which was likely boosted by one-off factors that are expected to fade in the final months of 2023. One might therefore deduce that this leaves the Fed in a neutral position as far as the outlook is concerned and a pause in September and beyond is justified.

Fed is fearful of overtightening

However, there are two significant unknowns here. One is the extent of the effects from the existing tightening that haven’t been felt yet. The other is whether energy prices will rally further, making inflation even stickier than it already is.

The Fed has become very mindful of the transmission lag of policy tightening during the course of 2023, downshifting the pace of rate increases contrary to data suggesting otherwise. The policy lag has been the main argument of the more dovish leaning FOMC members. Chair Jerome Powell falls into this camp.

But with real interest rates turning positive as all inflation metrics drop below 5% and the Fed funds rate reaches the 5.25%-5.50% range, the hawks are also increasingly confident that policy is restrictive enough. Thus, regardless of whether the Fed hikes one more time or not this year, the end of tightening is just around the corner.

Will new dot plot embrace higher for longer?

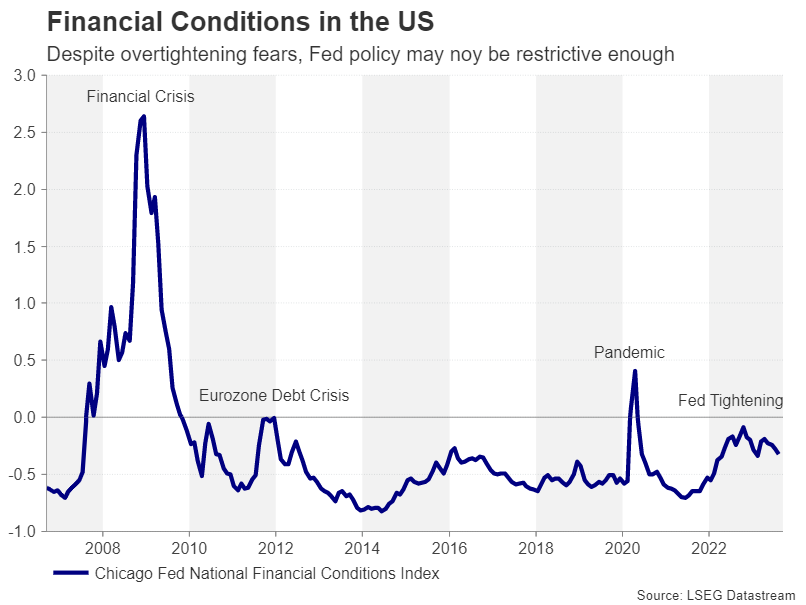

The question now is if the economy will slow at an alarming enough pace to trigger a wave of rate cuts. Some indicators, such as the Chicago Fed’s National Financial Conditions Index imply that financial conditions may not be tight enough. This raises the possibility of a resumption of rate hikes at some point in the future, even without a fresh acceleration in energy prices. At the very least, there remains a strong case for ‘higher for longer’.

However, markets have yet to be convinced as traders have about a 90-basis-point worth of rate cuts priced in. A pricing out of those cuts would not happen overnight and is potentially more of a 2024 story, but the process could start this week if FOMC members revise up their median projection of where they see rates in the next couple of years.

In the June dot plot, the median projection for 2024 was 4.6% and for 2025 it was 3.4%. If the Fed sees rates a lot higher in 2024 in the updated dot plot than in June, this would add more fuel to the US dollar’s latest uptrend.

Dollar’s bullish streak may not be over

Sending a clear signal on higher for longer would be one way for the Fed to possibly compensate for not committing to a final rate hike this year. The recent data has been neither too strong nor too soft, so keeping the option for a further rate rise on the table without pre-committing to it seems like a sensible middle-of-the-road approach.

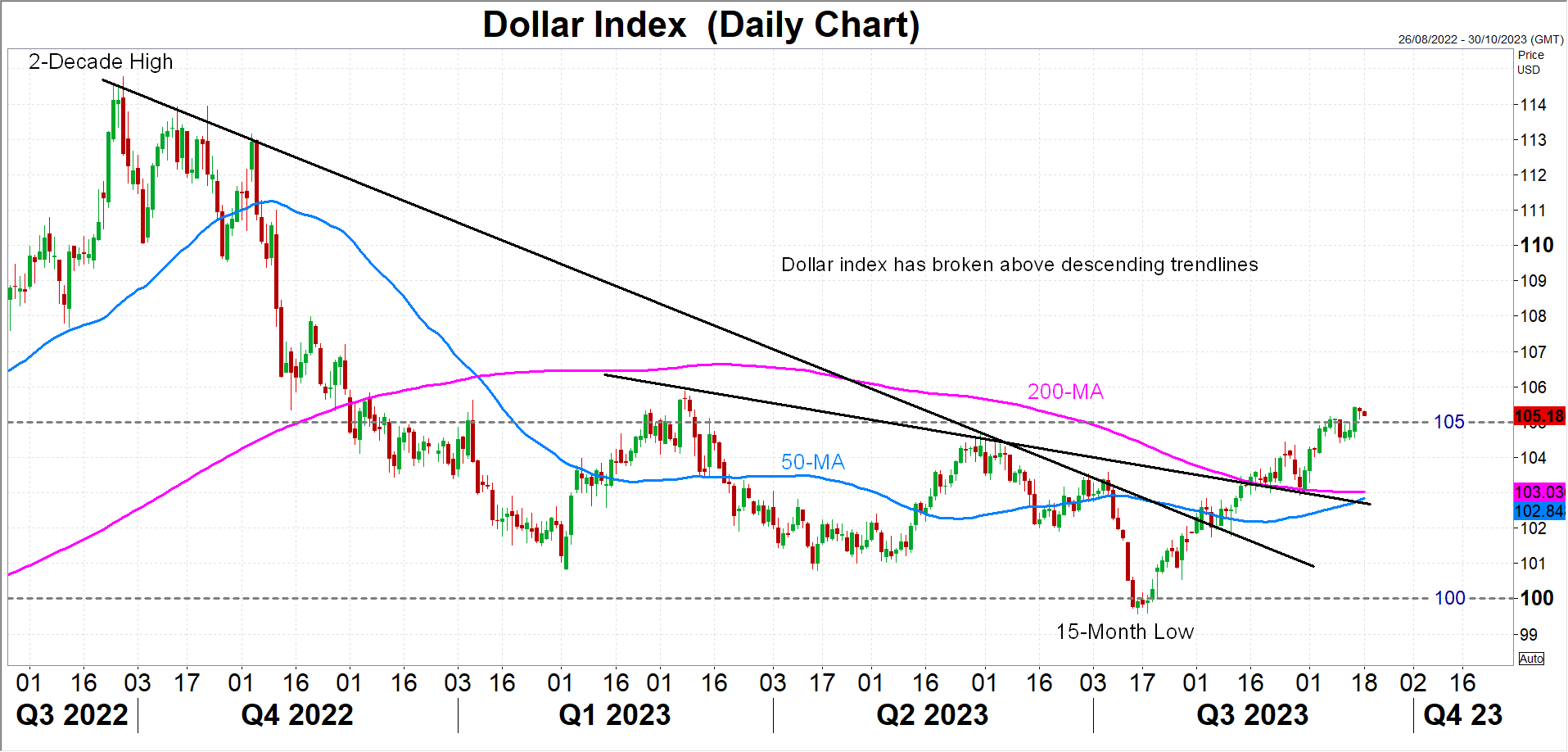

For the dollar, the most bullish outcome is if the Fed hints at a good chance for another hike as well as raises its projected rate path. This could push the dollar index past the March peak of 105.88, extending its winning streak.

However, the recent rally also exposes the greenback to a corrective selloff should the rate path not be revised up substantially, if at all, and Powell sounds upbeat on the prospect of inflation returning to the 2% target over the medium term in his press conference. The dollar index would be at risk of tumbling towards its 200-day moving average around 103.00 in such a scenario.