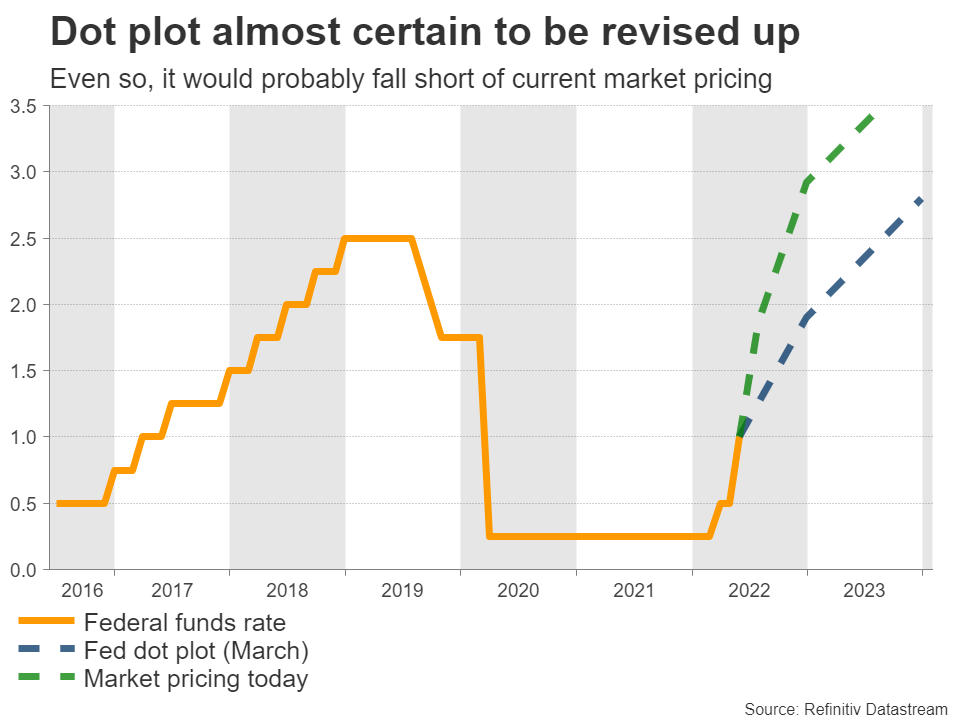

Fed to keep options open

The Federal Reserve has long telegraphed a 50 basis points rate increase for Wednesday’s meeting, and another one of equal size next month. Markets have done their part and have fully priced in both moves, which means the reaction in the dollar will boil down to Chairman Powell’s comments and the updated interest rate projections in the ‘dot plot’.

It’s pretty clear the US economy has started to lose momentum. Consumers are getting squeezed by rising living costs and are drawing down on their savings to compensate, the housing market is under stress amid soaring mortgage rates, and corporations are warning they might lay off workers as they try to defend profit margins.

But none of this will stop the Fed from delivering the two summer hikes it has committed to. Inflation is simply too high right now and the central bank has to act, despite signs the economy is slowing. The question is what happens in September and beyond - will the Fed keep its foot heavy on the brakes or is a ‘pause’ possible in case inflation cools or recession risks intensify?

Most likely, the Fed won’t signal anything concrete. Policymakers always prefer to keep their options open and wait for incoming data to guide their decisions. They’ve already outlined their summer plans - that’s enough for now. The interest rate forecasts in the dot plot will inevitably be revised higher, but are unlikely to exceed current market pricing.

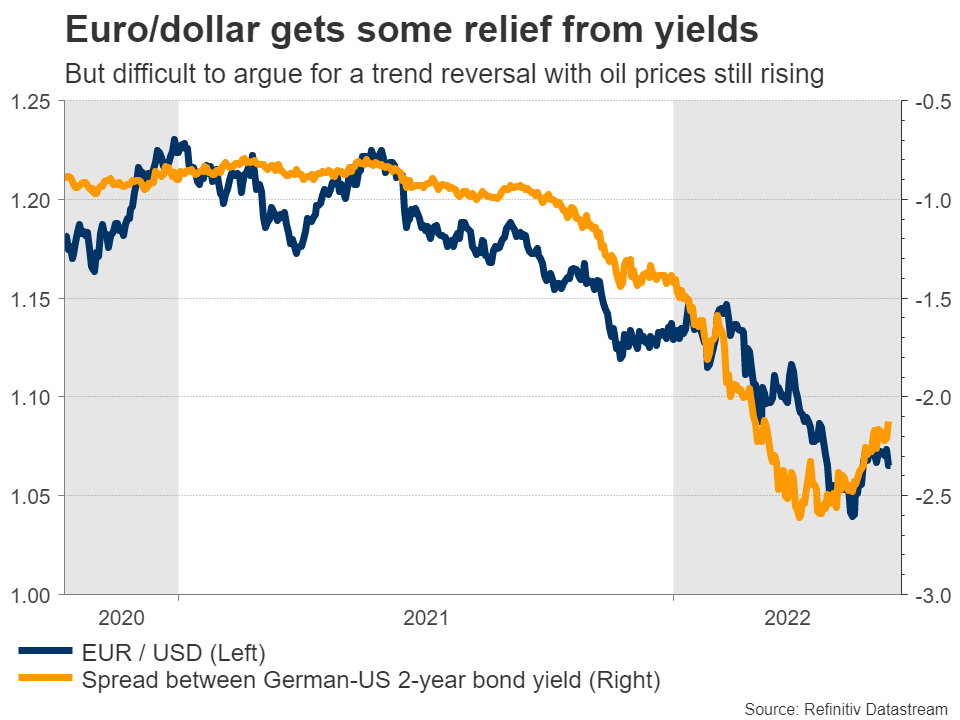

As for the dollar, it’s difficult to call for a trend reversal while every other major currency is in the gutter. The euro is suffering at the hands of soaring energy prices, the yen has been slaughtered by the Bank of Japan’s refusal to tighten, and the British pound is trading like a proxy for unstable stock markets. Not to mention that panic about a recession usually drives capital flows into the reserve currency.

In other words, the dollar won’t fall out of favor until the economic outlook for the rest of the world starts to improve. The nation’s retail sales for May will be released a few hours ahead of the Fed decision.

BoE - A hesitant rate hike

The Bank of England will conclude its own meeting on Thursday. A quarter-point rate increase is already fully priced in, and money markets also assign a 30% chance for a bigger, half-point move. Admittedly, a bigger move would not make much sense.

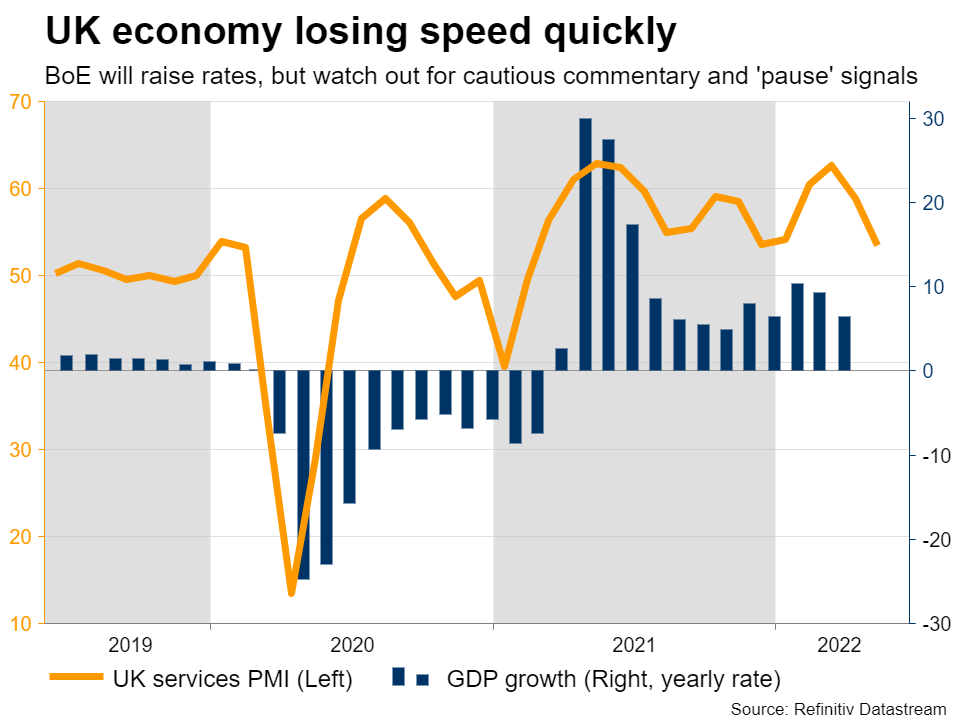

At its meeting last month, the BoE was already on red alert about recession risks. Some officials even supported a ‘pause’ in rate increases moving forward despite high inflation. Since then, their concerns were validated by incoming data, with business surveys signaling a sharp slowdown in the economy.

The BoE has not raised interest rates by 50 basis points so far in this cycle when the sun was shining - why would it do so now that storm clouds are on the horizon? This spells downside risks for sterling on the decision, as those looking for a bigger move are left disappointed.

In fact, market pricing seems way too aggressive right now. Six quarter-point rate increases are priced in over the next five meetings, so there’s plenty of scope for those bets to be dialed back, especially if the BoE emphasizes that a pause is possible.

Heading into the meeting, the nation’s GDP stats for April will be released on Monday ahead of the latest jobs report on Tuesday.

SNB - In the ECB’s shadow

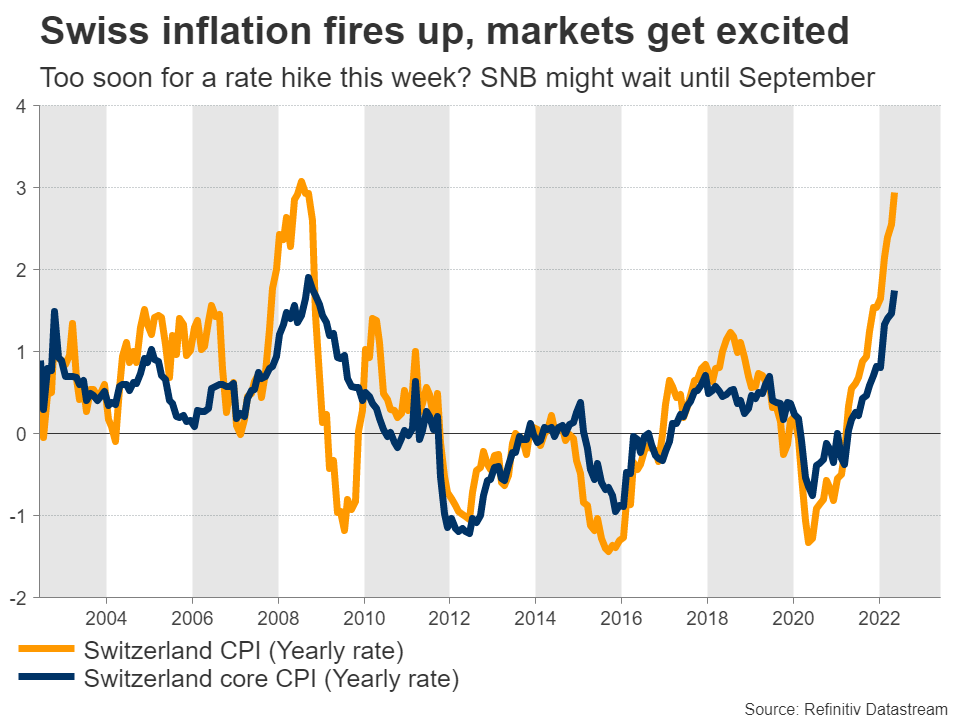

Over in Switzerland, the central bank will also announce its decision on Thursday and it will be the most important one in many years as markets imply a 70% chance for an immediate rate increase.

Inflation has finally accelerated and is running at the fastest pace in 14 years, although most of that reflects soaring energy and food costs. Wage growth remains subdued, which means there’s no real danger of a wage-price spiral that keeps feeding inflation and therefore no real urgency to raise rates.

Waiting until the next meeting in September to begin the hiking cycle seems more appropriate, as that would also allow the SNB to stay one step behind the European Central Bank, preventing any excessive appreciation in the franc.

BoJ refuses to join party

The only major central bank that is not even thinking about raising interest rates is the Bank of Japan, which will wrap up its meeting on Friday. A parade of BoJ officials made it very clear lately that policy changes are not on the agenda for this meeting.

That dealt another blow to the devastated yen. By holding their ground and allowing the yen to weaken so much, BoJ officials hope to import enough inflation from abroad to lift inflation expectations in an economy that has been battling deflation for decades.

But everything has limits. The yen’s collapse has become a political issue and with inflation already above its 2% target, there’s tremendous pressure on the BoJ to change course. While nothing is likely to happen this time, don’t be surprised if the BoJ begins to turn the ship around by July or September if inflation keeps accelerating. That could finally mark the bottom in the yen.

Finally in the commodity currency spectrum, Australia’s jobs report for May and New Zealand’s GDP growth stats for Q1 will both be released on Thursday.