Dollar loses its shine

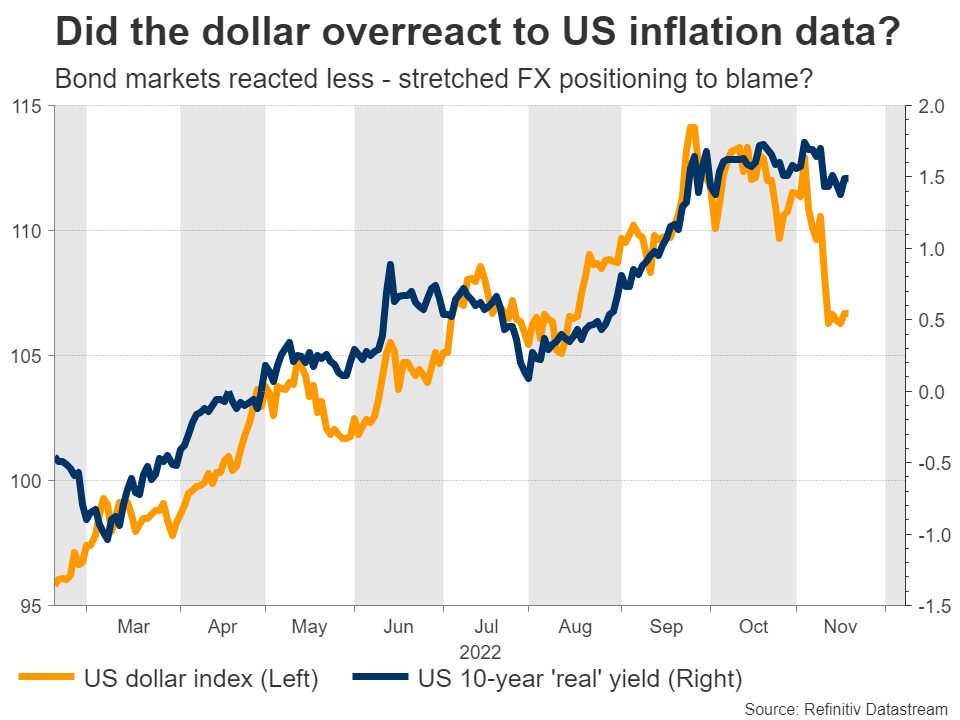

Signs that US inflation is finally simmering down dealt a heavy blow to the US dollar lately, as traders unwound bets that the Fed will raise rates beyond 5%. Admittedly though, the sharp FX moves seem like an overreaction, driven by one-sided positioning in ‘long dollar’ bets.

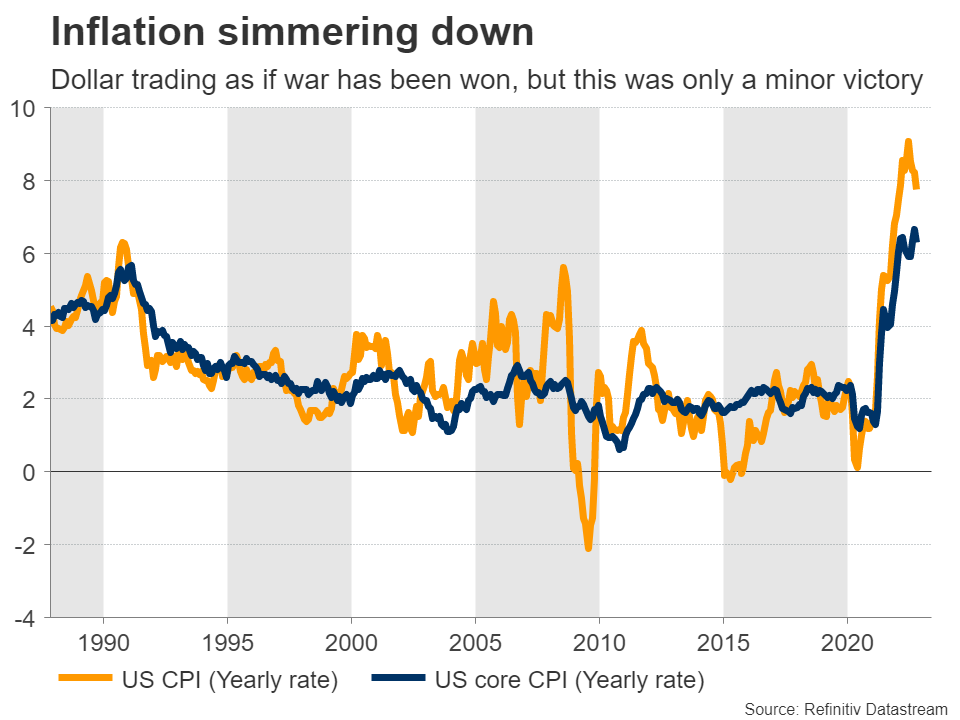

In a nutshell, the story around the Fed hasn’t changed enough to warrant such dramatic moves. The dollar is trading as if the war against inflation is about to end, but Fed pricing and US yields suggest this was only a minor victory. Inflation is still running at nearly four times its target, the labor market is in good shape, and consumption hasn’t slowed yet.

In other words, it’s still premature to be trading a Fed pivot. While inflation has likely peaked, there’s no telling how quickly it will come down. Fed officials have been adamant that even when they stop raising rates, they’ll keep them high until they are certain inflation has been crushed.

Markets will get an update on how inflationary pressures and the broader US economy are evolving on Wednesday, with the S&P Global business surveys for November. In recent months, the story has been that inflationary forces are retreating but mostly because demand is collapsing.

Later on Wednesday, the minutes of the latest FOMC meeting are out. They are outdated, as this meeting took place before the bombshell inflation report and we’ve heard from almost every FOMC official since then, but markets always find a way to react to this release. The overall message will likely be one of ‘determination’, which could give the dollar a small boost.

Overall, the dollar is at a crossroads. Most of the elements that fueled this stunning rally over the last two years seem to be losing their kick, with inflation cooling off and the Fed shifting into lower gear, yet it’s still too early to call for a proper trend reversal.

Even though the narrative around other major currencies has improved somewhat lately, for instance with European energy prices declining sharply, most foreign economies are likely to fall into recession long before America does. Hence, while the dollar rally is likely in its last chapters, it might have one ‘last hurrah’ left.

RBNZ - A split affair

Over in New Zealand, the Reserve Bank will wrap up its meeting early on Wednesday. Market participants are currently split on whether rates will be raised by 50 or 75 basis points. It is priced almost as a coin toss, leaning slightly towards the smaller move.

Investors think the RBNZ might play it cautious because it hasn’t raised rates by 75 bps so far and other central banks have slowed down their tightening pace lately, for instance in neighboring Australia. However, that might be a miscalculation this time.

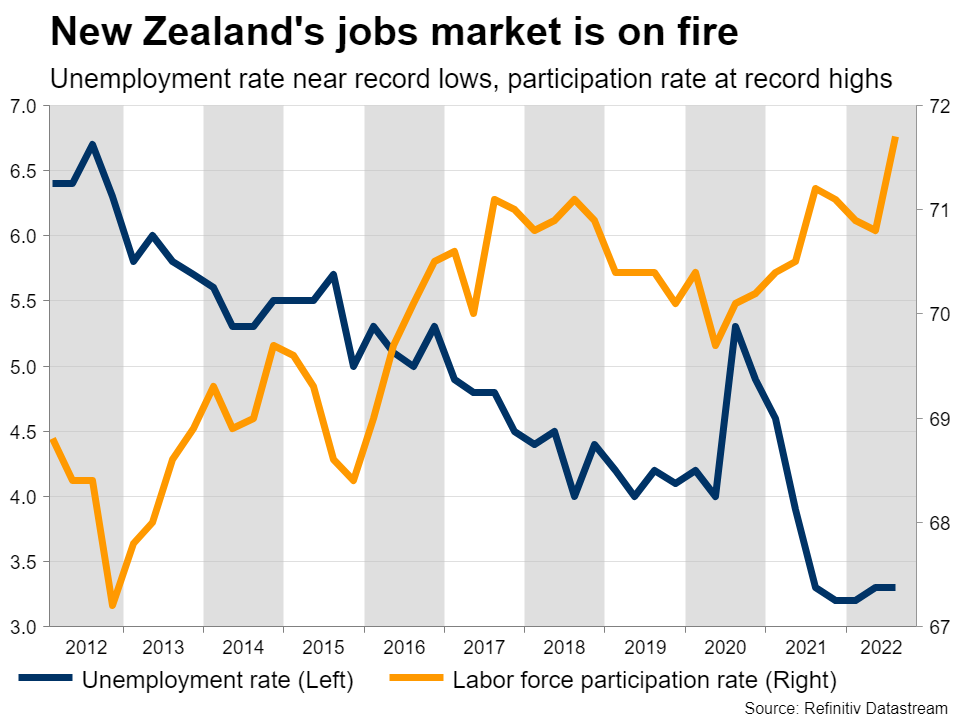

Since the RBNZ last met, a string of powerful data releases suggested the economy is running much hotter than policymakers anticipated. For starters, inflation far exceeded the central bank’s forecasts during the third quarter, while the jobs market went gangbusters, with the unemployment rate holding near record lows even as labor force participation hit new all-time highs.

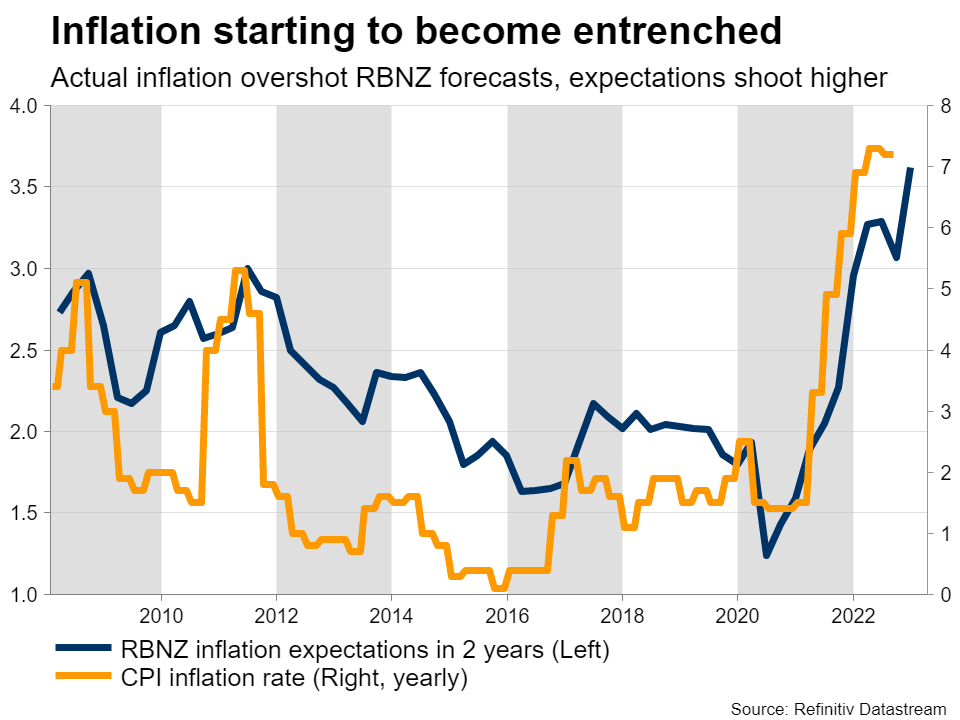

Most importantly, the RBNZ’s own 2-year inflation expectations metric shot higher, indicating that inflationary pressures are becoming entrenched. This was further reaffirmed by an acceleration in wage growth. Of course, there are risks too. House prices have fallen more than 10% from last year, while the sharp slowdown in China is a huge threat for exports.

Still, the balance of evidence points to a 75 bps move as the most prudent option, an outcome that could temporarily boost the kiwi. If it’s a 50 bps move instead, it will likely be accompanied by ultra-hawkish commentary, limiting the currency’s losses.

Eurozone and British PMIs

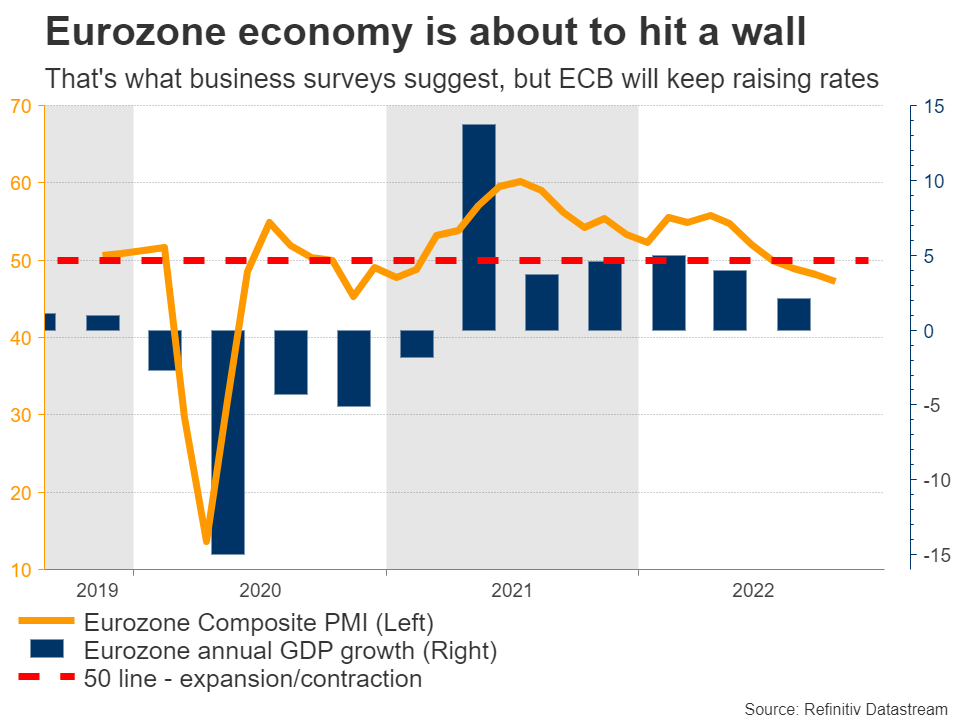

In the Eurozone and United Kingdom, all eyes will be on the latest PMI business surveys on Wednesday. Forecasts point to another decline in these indices, which would add credence to concerns that both economies are either already in recession or heading directly for one.

With inflation running at double digits, markets are still leaning towards a 75bps rate hike from the ECB next month, despite clear signs that growth is crumbling. In fact, the latest forecasts from the European Commission suggest the economy will begin to contract this quarter already.

On the bright side, the sharp decline in energy prices suggests this recession won’t be as brutal as initially feared, which is encouraging for the euro, but not a game changer. A sustainable rally would require signs of improving growth or good news from Ukraine, neither of which is on the table for now.

As for sterling, the outlook is even darker. Both the government and Bank of England expect a prolonged recession, which the latest austerity budget will likely deepen.

Meanwhile, the nation’s twin deficits are still massive and require funding, leaving the pound exposed to global risk sentiment. That’s a toxic cocktail, as equity valuations remain stretched and earnings estimates are still overly optimistic (see here).

Finally in Japan, the forward-looking Tokyo CPIs are out on Friday, and will be crucial in helping investors decide whether the Bank of Japan will adjust policy next month.